Have you ever wondered how we plan to fund the opening of our full service grocery store? Board Treasurer, Tom Lamberty, has all the financial details for you here!

Prairie Food Co-op follows a well-established process to open our store. The foundation of everything is growing the number of Owners. At 800 Owners, we have the proven support to sign a lease, announce the site of our store, and begin the search for the store’s General Manager. At 1,000 Owners, we will launch our owner loan campaign that will give Owners a unique opportunity to invest in their community. On opening day, we project to have 1,500 Owners.

After completing a market study, business plan, and financial pro-forma it is clear that opening a 10,000 square foot grocery store is a major financial undertaking, but one that we can achieve. This newsletter explains each upcoming expense category and all expected sources of revenue needed to open our store. The delicate fiscal balance between Sources and Uses motives the Board to move cautiously, but steadily, forward.

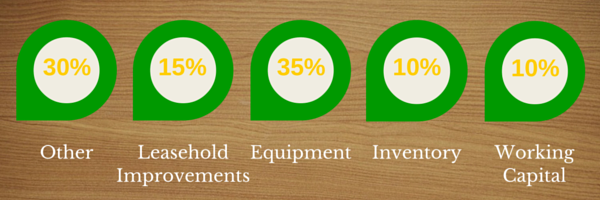

Expenses (Uses of Funds)

Opening a new grocery store requires numerous upfront expenses. We have broken down our anticipated costs into four main categories and one catch-all for the rest.

| Equipment | Equipment necessary to make the space function as a grocery store. Includes storage and shelving, refrigeration and cooling, cash registers, and back-office computer systems. |

| Leasehold Improvement | Alterations made to rental premises in order to customize it for a full service grocery store. Includes painting, installing partitions, changing the flooring, customized light fixtures, upgrades to electrical and plumbing, and so on. |

| Working Capital | Cash available to pay debts. The margin of protection we will give our short-term creditors. |

| Inventory | All the amazing products that will fill our shelves. Includes pre-packaged foods, store-made foods, dairy, produce, meat, and non-food items. |

| Other | A variety of other expenses. Includes staffing and administration, lease deposit, promotion, and professional fees. |

Revenue (Sources of Funds)

We must pay for all the expenses highlighted above either before the store opens or as we phase in the opening of future store departments. As a cooperative business, we are restricted by law from certain common funding sources. We can’t raise money through venture capital because we are an Ownership organization; we can’t raise money through grants because we are not a 501(c)(3) organization. We have to create our own funding path. Co-ops are funded through a combination of crowd-sourced capital and financing. See how it all breaks down below.

| Owner Equity | Money paid by Owners to purchase Ownership shares |

| Preferred Shares | State of Illinois investors may purchase Preferred Shares of Prairie Food Co-op stock with various dividend rates |

| Owner Loans | Loans made by Owners to the co-op under a variety of competitive interest rates |

| Bank Loan (NCB) | We are relying on the National Cooperative Bank (NCB) to provide financing in the form of a traditional bank loan. |

| Non-traditional Financing | Local sources of financing from foundations and community programs |

| Grants/Other | Government grants and other sources |

The most significant chunk of our revenue will be Preferred Shares and Owner loans, at about 40%. Preferred Shares and Owner loans are a fundamental method of funding for modern food co-ops. It is also another way the co-op benefits our community, one lender at a time. Owners will have the opportunity to make loans to the co-op. While the return of the principal is long-term, each owner/lender will earn interest under a variety of competitive interest rates. Generally, the longer you are willing to wait to get your principal back, the more you will be eligible to earn in annual interest. Thanks to a recent change in the Illinois Cooperative Act, the co-op can now also sell Preferred Share stock to any State of Illinois investor. This greatly expands the co-op's ability to raise funds from socially minded investors, as well as provides investment opportunities for those looking for social and community investment options.

Preferred Shares and Owner loans are essential because the funds generated by them are viewed by traditional lenders as capital rather than as liabilities. See, when individuals are willing to personally invest in a business that benefits the community at large it is evidence that people are excited about this store and are more likely to shop there! When banks and other outside lenders see that we have at least 50% of our capital internally from Owners (share purchases and loans) the co-op will be seen as a financially sound investment for them as well.

Extra Credit: Do you know total anticipated cost to open Prairie Food Co-op (or any grocery store of our size)? To construct a beautiful, modern grocery store with the products and services that consumers expect, it will cost approximately $3 million. Could we do it cheaper? Perhaps, but that has proven to be a critical factor in a store's ability to succeed. And we fully expect Prairie Food Co-op to serve our community far into the future!

We are as eager as our owners and the community at large to open a new grocery store in Lombard. Thank you again for your efforts to help us reach that goal! As always, please contact us with any questions.

Board of Directors, Prairie Food Co-op